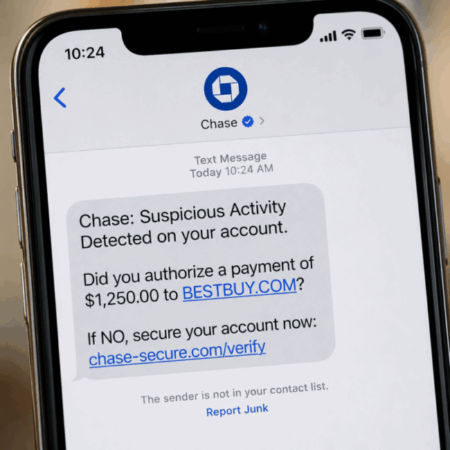

A text arrives. Chase Bank. Suspicious activity. Click here to secure your account.

She clicked.

The woman in question — a former bank teller who’d literally watched other customers fall for this exact scheme — entered her login credentials, possibly her Social Security number, and hit submit. By the time her daughter got the tearful phone call, $167,000 in wedding savings and decades of retirement planning were sitting in the crosshairs.

The daughter’s letter to the Daily Mail reads like a controlled scream — equal parts terror, confusion, and the kind of helpless rage that comes from watching someone you love step on a landmine in real time. She’s not wrong to be scared. Phishing scam recovery isn’t a clean process, and the window between “no money missing yet” and “checking account drained” can close faster than you’d think.

The Anatomy of a Fake Bank Text

Here’s what makes these scams so effective: they don’t look like scams anymore.

The fake Chase text included urgency (“account locked”), a plausible threat (“suspicious activity”), and a link that probably mirrored the bank’s actual URL down to the font choice. No typos. No obvious red flags. Just a message designed to trigger the exact response it got — immediate compliance.

Todd Spodek, a federal criminal defense attorney who handles wire fraud cases, told the Daily Mail he sees this pattern constantly. Romance scams, fake job offers, shipping notifications — the tactics shift, but the goal stays the same. Get someone to voluntarily hand over their credentials while their brain is still in fight-or-flight mode.

Pew Research found that 73% of American adults have dealt with credit card fraud, ransomware, or online shopping scams. The FTC notes that Gen X, Millennials, and Gen Z are 34% more likely than older adults to lose money to fraud. This isn’t an “elderly people don’t understand technology” problem — it’s a “panic overrides logic” problem, and it scales across demographics.

What Actually Happens After You Click

The daughter’s instinct — that “no money missing yet” doesn’t mean safety — is correct.

Cybercriminals move fast once they have access. They’ll often test small transactions first (a $10 charge to see if the account’s live), then escalate to savings withdrawals or wire transfers. Even if the checking account looks untouched, the clock is running.

Spodek’s advice: assume the information is already exposed. Contact the bank’s fraud department immediately. Lock down all accounts tied to that login. Change every password. Enable transaction alerts so any movement triggers a notification.

The good news — if there is any — is that banks are often required to reimburse unauthorized transactions if the fraud is reported quickly. Chase confirmed to the Daily Mail that victims should “discontinue all contact with the scammer immediately, take note of all relevant information, and contact your bank.”

The bad news: if the victim was tricked into voluntarily sending money (via Zelle, Venmo, or cash), the odds of recovery drop to nearly zero. The bank can’t reverse a transaction you authorized, even if you were deceived.

The Bigger Risk: What Else Is Exposed

The daughter’s panic about retirement accounts and stock portfolios isn’t unfounded, but those assets are harder to access than checking and savings. Spodek recommends notifying those institutions anyway and flagging the situation as a precaution.

The real vulnerability is identity theft. If the mother entered her Social Security number — and she “can’t remember” if she did, which probably means she did — the exposure extends beyond bank accounts. Scammers can open new credit lines, file fraudulent tax returns, or sell the data to other criminals.

Freezing credit with Equifax, Experian, and TransUnion is non-negotiable. Filing a report with the Federal Trade Commission creates a paper trail. Both steps add layers of protection that might stop secondary fraud before it starts.

Why “She Should Have Known Better” Misses the Point

The daughter mentions her mother’s background as a bank teller — someone who’d seen customers fall for scams firsthand. That detail makes the story feel more absurd, but it also underscores the real mechanism at work here.

Scams don’t succeed because people are stupid. They succeed because they’re designed to short-circuit rational thinking. Urgency. Fear. A message that looks exactly like the real thing. The brain doesn’t have time to fact-check when it thinks the house is on fire.

Chase’s advice is simple: don’t click the link. Go directly to the official app or website. If there’s a real problem, it’ll show up there. If there isn’t, you’ve just avoided handing your credentials to someone who’ll drain your accounts before you finish breakfast.

Spodek echoes this: “Whether it’s a fake bank alert, a delivery notice, or a message that appears to come from someone you trust, the safest approach is always the same. Do not click the link.”

What Comes Next

The daughter’s question — “What should we expect next?” — doesn’t have a clean answer.

If the mother acted fast enough, the damage might be contained. If the scammers got in before she locked things down, the next few days will involve a lot of phone calls, fraud reports, and the slow, grinding work of recovering from phishing scams.

Chase also warns that scammers often target the same victim twice. They know someone who fell for it once might fall for it again — especially if the second message claims to be “fraud protection” following up on the first incident.

The $167,000 wedding fund might survive this. The retirement accounts might stay intact. But the lesson — that even people who “should know better” can be duped when the pressure’s on — is already locked in.